ANZ Australia changes its housing forecast

2023-08-22

Another bank has changed its housing forecast.

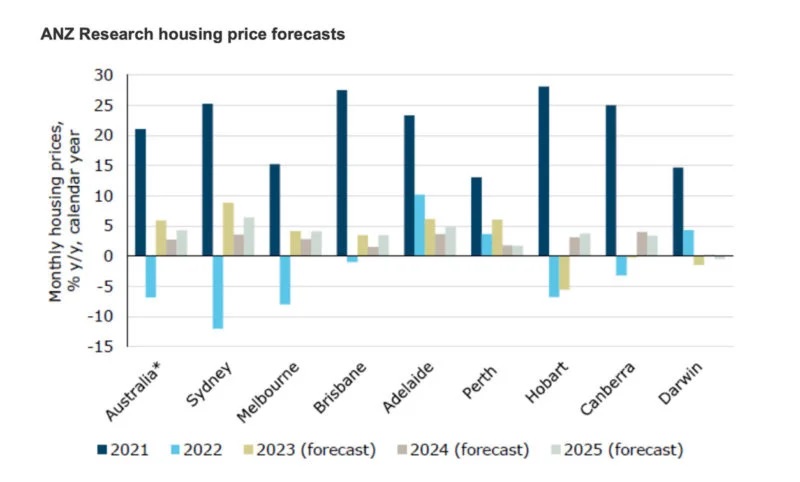

ANZ Bank now expects housing prices in Australia to rise 5-6% in 2023.

In 2024, they expect growth to slow to around 3%, reflecting rising unemployment and the lagged impact of past rate hikes as well as slower population growth.

Then the ANZ expects housing prices to reaccelerate to around 4-5% in 2025 supported by a modest cut in interest rates.

What a turnaround!

The year began with a plethora of predictions from the senior economists of all our Big 4 banks, and they all suggested property prices would fall in 2023.

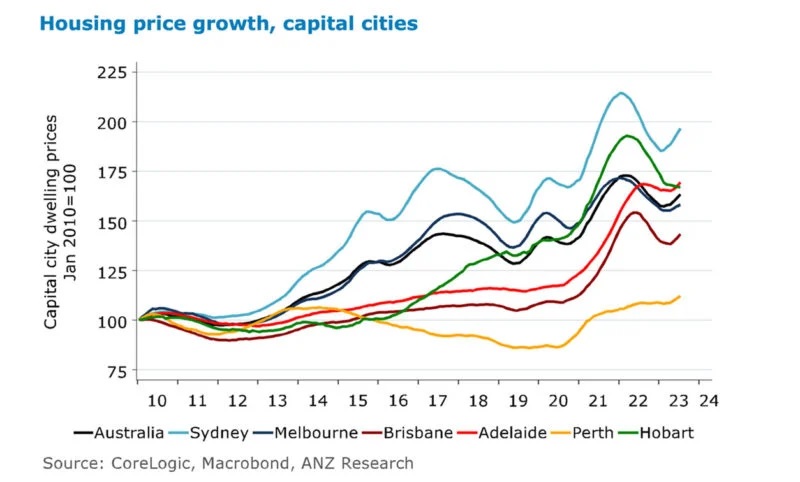

Yet Australia’s housing markets continued to defy their expectations!

Despite 12 interest rate increases from the Reserve Bank of Australia, which have seen official rates rise by 4 per cent over the last year, property prices not only stopped falling, but they have now been on the rise for six months.

The peak-to-trough change in Australian house prices was 9 per cent according to CoreLogic, and only 4 per cent according to PropTrack, which is confusing those analysts who were looking for prices to drop by 15, 20, or even 30 per cent on the back of interest rate increases.

But now it's clear that our property markets have bottomed and we have moved into the next phase - the recovery phase - of the property cycle.

Lower listing volumes (fewer properties for sale) are helping protect the market from further downward pressure.

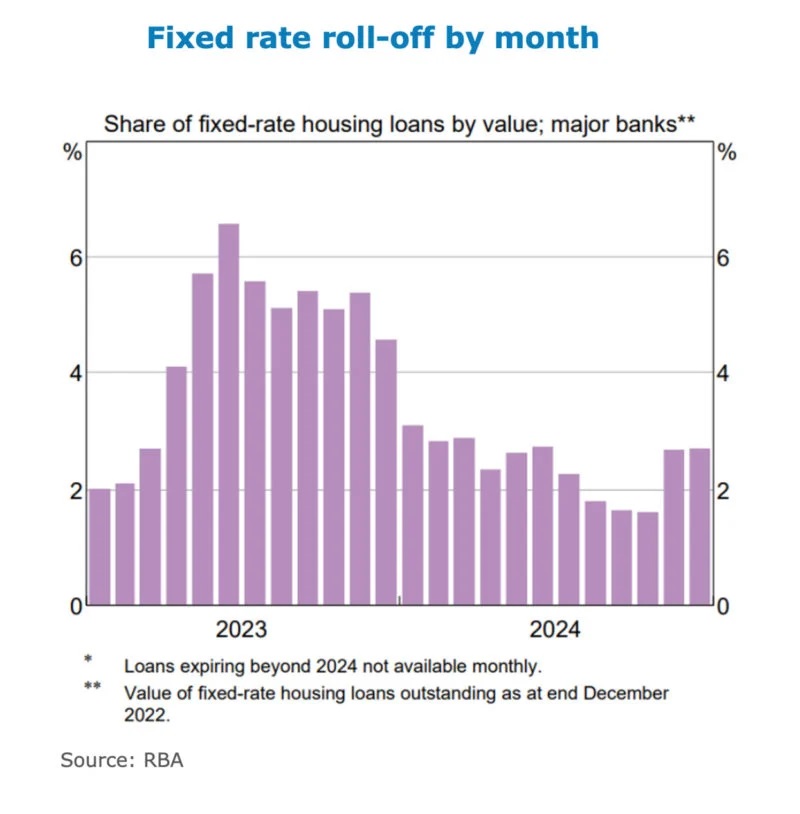

While many are concerned about a "fixed rate cliff" ahead, RBA data indicates the majority of mortgage debt is on variable terms.

Many people have also been overpaying on their mortgages during the low interest rate cycle, while many others have already refinanced.

Inflation has now peaked and it's likely so have interest rates, and in due course consumer confidence will return and the markets will continue their upward trajectory.

ANZ says that the impacts of housing shortages and tight rental vacancies are currently outweighing the impacts of cash rate increases.

According to the ANZ, forward indicators including housing finance approvals and auction clearance rates suggest further housing price increases for the balance of this year.

What about the fixed rate cliff?

ANZ explains that the cash rate has risen 4% since May 2022 to 4.1%, but strong refinancing activity and competition have limited the pass-through to average new mortgage rates, which have risen by less than 4%.

The bank suggests that fixed-rate loans have sheltered some households from the financial impacts of higher rates.

Yet the current monthly rate of expiring fixed loans is near its peak and this is squeezing some household cashflows and may be causing falling excess mortgage repayments.

The share of income going to housing payments is expected to reach a record high of around 10%.

This is undermining the confidence of indebted households, though ANZ expects arrears rates to remain low.

The ANZ note that consumer confidence has been very weak since mid-2022, particularly for homeowners with a mortgage.

High-interest payments and inflation have reduced the ability of many households to make extra loan repayments though making during periods of low interest rates.

However, they did notice that many households still retain strong financial buffers.

ANZ Bank now expects housing prices in Australia to rise 5-6% in 2023.

In 2024, they expect growth to slow to around 3%, reflecting rising unemployment and the lagged impact of past rate hikes as well as slower population growth.

Then the ANZ expects housing prices to reaccelerate to around 4-5% in 2025 supported by a modest cut in interest rates.

What a turnaround!

The year began with a plethora of predictions from the senior economists of all our Big 4 banks, and they all suggested property prices would fall in 2023.

Yet Australia’s housing markets continued to defy their expectations!

Despite 12 interest rate increases from the Reserve Bank of Australia, which have seen official rates rise by 4 per cent over the last year, property prices not only stopped falling, but they have now been on the rise for six months.

The peak-to-trough change in Australian house prices was 9 per cent according to CoreLogic, and only 4 per cent according to PropTrack, which is confusing those analysts who were looking for prices to drop by 15, 20, or even 30 per cent on the back of interest rate increases.

But now it's clear that our property markets have bottomed and we have moved into the next phase - the recovery phase - of the property cycle.

Lower listing volumes (fewer properties for sale) are helping protect the market from further downward pressure.

While many are concerned about a "fixed rate cliff" ahead, RBA data indicates the majority of mortgage debt is on variable terms.

Many people have also been overpaying on their mortgages during the low interest rate cycle, while many others have already refinanced.

Inflation has now peaked and it's likely so have interest rates, and in due course consumer confidence will return and the markets will continue their upward trajectory.

ANZ says that the impacts of housing shortages and tight rental vacancies are currently outweighing the impacts of cash rate increases.

According to the ANZ, forward indicators including housing finance approvals and auction clearance rates suggest further housing price increases for the balance of this year.

What about the fixed rate cliff?

ANZ explains that the cash rate has risen 4% since May 2022 to 4.1%, but strong refinancing activity and competition have limited the pass-through to average new mortgage rates, which have risen by less than 4%.

The bank suggests that fixed-rate loans have sheltered some households from the financial impacts of higher rates.

Yet the current monthly rate of expiring fixed loans is near its peak and this is squeezing some household cashflows and may be causing falling excess mortgage repayments.

The share of income going to housing payments is expected to reach a record high of around 10%.

This is undermining the confidence of indebted households, though ANZ expects arrears rates to remain low.

The ANZ note that consumer confidence has been very weak since mid-2022, particularly for homeowners with a mortgage.

High-interest payments and inflation have reduced the ability of many households to make extra loan repayments though making during periods of low interest rates.

However, they did notice that many households still retain strong financial buffers.

- *E-mail:

- *Cel:

- *Password: